MARTINGALECALCULATOR.COM

MARTINGALECALCULATOR.COM

Responsibility is limited to correctness of the simulation logic, fidelity to the stated probabilistic model assumptions, and methodological integrity of the resulting probability measures.

RISK OF RUIN IN MARTINGALE BETTING SYSTEMS

This document presents a constraint analysis of risk of ruin under a fixed probabilistic model for a martingale betting system. Risk of ruin is treated strictly as a property of the mathematical model, not as a statement about outcomes in any specific real-world setting.

The scope is definitional and interpretive only. It explicitly excludes advice, instruction, optimization, behavioral recommendations, or practical guidance. The purpose of this page is to define what “risk of ruin” means within the model, how it arises structurally, and how it constrains interpretation of simulated results.

Definition of Risk of Ruin

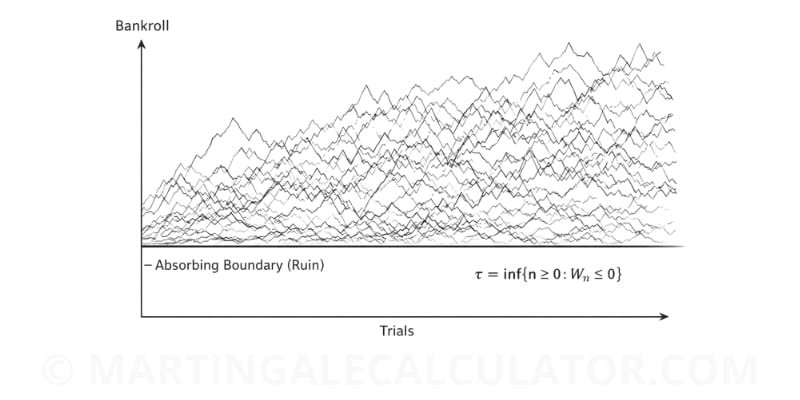

Risk of ruin is defined as a probability measure over a stochastic process that represents capital evolution under repeated trials. Let {Wn}n≥0 denote a discrete-time process representing available capital, with initial capital W0 fixed and finite.

Ruin is defined as an absorbing boundary at bankroll depletion, represented by the state Wn ≤ 0. Absorption means that once this boundary is reached, the process is terminated for the purpose of the model and does not resume. Formally, define the ruin time as the stopping time:

τ = inf{n ≥ 0 : Wn ≤ 0}

Risk of ruin over a finite time horizon N is the probability:

P(τ ≤ N)

under the model’s probability law. Long-run risk of ruin refers to the asymptotic behavior of

P(τ < ∞)

as the time horizon increases without bound, when such a limit is well-defined within the assumed process class.

This definition is intentionally agnostic to any narrative description of trials. It depends only on the existence of a well-specified transition rule for {Wn}, a probabilistic mechanism generating trial outcomes, and an absorbing boundary representing bankroll depletion.

Structural Origin of Risk in Martingale Models

Within the model, risk of ruin arises from the interaction between exponential stake progression and finite capital. A martingale betting system is characterized by deterministic stake updates that increase multiplicatively following adverse outcomes. This progression is not incidental. It is the defining structural feature of the system.

Finite bankroll constraints impose a hard limit on loss sequence tolerance. The stake sequence implied by exponential progression produces a capital demand that grows faster than any linear accumulation of buffer. For any fixed initial capital and fixed progression rule, there exists a finite loss sequence length at which the required stake exceeds remaining capital.

This implies that bankroll depletion is reachable under a finite sequence of adverse outcomes, without requiring any additional modeling assumptions beyond the stake update rule and capital accounting.

Loss sequences are modeled as realizations of a stochastic process. Under independence and fixed probabilities, sequences of adverse outcomes have strictly positive probability at every finite length. The existence of a strictly positive probability for each finite loss sequence length is sufficient to establish that the ruin boundary is not a theoretical artifact. It is a reachable state implied by the model’s transition structure.

The resulting risk is therefore structural rather than situational. It is induced by exponential stake growth interacting with a bounded state space for capital. Constraint analysis in this context is the analysis of reachability and probability mass assigned to boundary-hitting events.

Mathematical Framing of Ruin Probability

The canonical abstraction is a sequence of Bernoulli trials with fixed success probability. Trial outcomes generate increments and decrements in {Wn} according to a deterministic stake function applied to the recent outcome history.

Under this framing, ruin probability is a tail probability. It is the probability that the realized path contains, within a specified horizon, an adverse segment sufficient to force the process to the absorbing boundary.

Tail risk is central because exponential progression assigns disproportionate capital impact to rare but long loss sequences. While the probability of observing a long adverse run decays with run length under fixed probabilities, the capital requirement grows exponentially with that same length. Ruin probability is therefore not determined by the probability of any single loss. It is determined by the distribution over sequences and by how the model maps sequences into capital consumption.

Variance accumulation matters because dispersion in cumulative outcomes increases with the number of trials. Even when expected drift is constrained by the model’s payoff mapping, dispersion is not eliminated by continuation. The process continues to sample from the distribution of sequences, and sampling increases the chance that an extreme segment occurs somewhere in the realized path. Expected value is often incorrectly treated as a stabilizing or protective property in this context. The distinction between long-run expectation and finite-path absorption is addressed explicitly in Expected Value in Martingale Systems, which defines how expected value must be interpreted within this model.

Risk of ruin is not a statement about a typical path. It is a statement about the measure of boundary-hitting paths under a specified probability law. The event is defined by absorption, not by short-run fluctuations that do not cross the boundary.

Time Horizon and Ruin Probability

Time horizon is a primary parameter in any ruin probability statement. For a fixed model, P(τ ≤ N) is non-decreasing in N. This monotonicity follows directly from event inclusion: the event of ruin by time N is contained within the event of ruin by time N+1.

As the horizon expands, cumulative exposure to loss sequences increases. The model does not require that adverse outcomes become more frequent. It requires only that additional trials create additional opportunities for adverse segments to appear. Under independence and stationarity, the distribution of finite sequences remains stable while the number of sampled subsequences increases with time.

Asymptotic behavior depends on the assumed process and constraints. In many martingale betting system specifications with finite bankroll and exponential progression, the absorbing boundary remains reachable with positive probability at every finite time. As a result, cumulative ruin probability may approach one as the horizon grows. This is an asymptotic statement about probability mass concentration, not a deterministic guarantee about any finite run.

A ruin probability reported for one horizon does not generalize to another horizon without recomputation. The time horizon is part of the event definition itself.

Survival Does Not Eliminate Ruin Probability

Continuation of the process up to a given trial count is a conditional statement, not a refutation of ruin risk. Conditioning on survival up to time n changes the distribution of the current state Wn and the recent outcome history. It does not remove the structural reachability of the absorbing boundary under future trials.

Survival bias arises when observed continuations are implicitly treated as representative of the full distribution of paths. In probabilistic terms, the set of surviving paths at time n is a subset selected by a boundary constraint. This selection alters which paths are observed but does not change the underlying probability law generating future outcomes.

Short-term continuation and long-run behavior are distinct objects. The former is an event defined over a finite prefix of trials. The latter concerns probability mass over all paths as the horizon expands. Constraint analysis maintains this distinction explicitly.

Model Assumptions and Constraint Scope

This document assumes fixed probabilities. Trial outcomes are generated from a time-homogeneous probability mechanism. There is no parameter drift, no state-dependent probability change, and no regime switching.

This document assumes independent trials. Outcomes are modeled as independent draws conditional only on fixed probability parameters. Dependence structures, clustering, or memory effects define different stochastic processes and are outside scope.

This document assumes no capital injection. The capital process {Wn} is closed under the model’s accounting rules. External additions to capital are excluded. Ruin is absorbing and permanent within the model.

This document assumes no adaptive behavior. The stake update rule is fixed and deterministic. It does not vary based on time, partial horizon remaining, or auxiliary policies. Adaptive strategies define different transition kernels and therefore different ruin probabilities.

These assumptions are constitutive. Risk of ruin is not a universal constant of a martingale betting system in the abstract. It is a probability measure defined under a specific probabilistic model. Violation of any assumption invalidates transfer of computed ruin probabilities.

Model Constraints Summary

| Constraint | Model Specification |

|---|---|

| Trial Independence | Each trial is modeled as independent with fixed probability parameters |

| Capital Flow | No external capital injections are permitted within the model |

| Boundary Condition | Bankroll depletion is treated as an absorbing state |

| Stake Rule | Stake progression is fixed and deterministic |

Relationship to the Martingale Calculator

The Martingale Calculator is an implementation of the model defined by explicit stake progression, fixed trial probabilities, and an absorbing boundary at bankroll depletion. This page defines the boundary conditions and probabilistic interpretation that constrain the calculator’s outputs.

The calculator provides computed measures under the stated assumptions. This document defines what those measures mean, and what they do not mean.

Scope Boundary

This page does not define parameter selection methods. It does not define stopping conditions, session design, or behavioral rules. It does not compare alternative systems, progressions, or policies. It does not interpret results as guarantees or prescriptions.

The document is non-prescriptive by construction. Its sole purpose is to constrain interpretation of risk of ruin as a probability of reaching an absorbing boundary under a specified stochastic process, and to document the limits of that specification.

A broader discussion of how Martingale systems are treated as abstract mathematical models, rather than behavioral guidance, is defined in the constraint page on martingale systems as mathematical models.