MARTINGALECALCULATOR.COM

MARTINGALECALCULATOR.COM

Kim Birch is a published author and analyst working with probabilistic systems, mathematical modeling, and regulated gambling frameworks. On martingalecalculator.com, his focus is on defining boundaries, assumptions, and constraints so that mathematical simulations are interpreted correctly and not mistaken for advice or behavioral guidance.

EXPECTED VALUE IN MARTINGALE SYSTEMS - MATHEMATICAL INTERPRETATION

Expected value is frequently misunderstood in progression systems. This page exists to prevent that misinterpretation. It explains expected value as a mathematical property of the model, not a measure of outcomes or decisions.

The article explains expected value as a mathematical property of the model, not a measure of outcomes or decisions.

What Expected Value Means in a Martingale Model

Expected value is a mathematical concept. In a Martingale system, expected value refers to the long-run statistical average of outcomes generated by the model under fixed assumptions. It is defined over repeated trials, not over individual sequences or finite sessions.

Expected value does not predict what will happen next. It does not describe what happens in a short sequence. It is not a forecast and it is not a guarantee. It exists as a property of the mathematical structure itself. Within a Martingale system, expected value is derived from the probability distribution of outcomes and the payoff mapping embedded in the model. Bankroll size, progression depth, or stopping conditions do not change this underlying expectation.

They affect survivability and termination, not the mathematical expectation itself. Understanding expected value correctly requires separating statistical averages from realized paths.

Expected Value Is a Property of the Model, Not the Player

Expected value belongs to the model, not to the individual interacting with it. This distinction is critical. In a probabilistic model, expectation is determined by assumptions about probabilities and outcomes. It does not respond to intent, discipline, timing, or persistence.

Changing parameters such as starting capital or progression limits does not alter expected value. These parameters affect how long the system can operate before termination, but they do not modify the expectation embedded in the structure.

This is a common point of confusion. It is tempting to believe that careful configuration can “improve” expectation. In mathematical terms, that belief is incorrect. Expected value remains fixed as long as the probabilistic model remains unchanged.

The Martingale system has a mathematical expectation regardless of how it is approached or configured.

Why Expected Value Does Not Describe Short-Run Outcomes

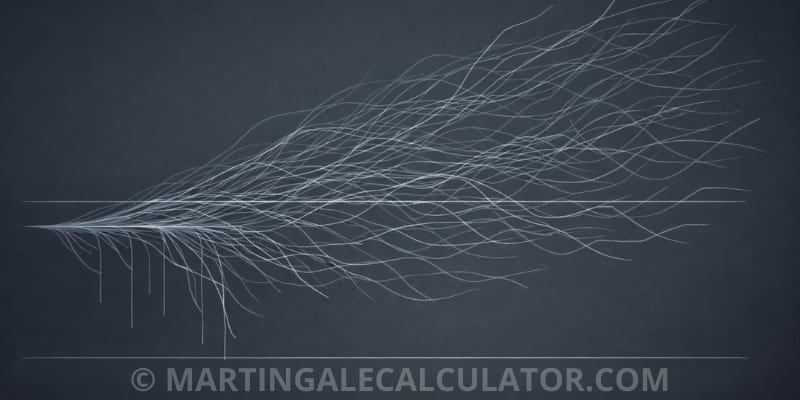

Expected value describes an average taken over a very large number of trials. Short-run outcomes are governed by variance. Variance measures dispersion, not direction. It explains why results can deviate significantly from expectation in limited samples.

In systems with high variance, short sequences can produce outcomes that appear to contradict expectation. This does not invalidate expected value. It demonstrates that expectation is not a short-run descriptor.

A negative expectation model can generate temporary positive sequences. A neutral expectation model can produce large deviations in either direction. These outcomes are statistically normal under variance.

Short-run results carry little interpretive weight. Expected value only becomes meaningful as repetition increases, and even then it describes an average, not a path.

Common Misinterpretation: “Near-Zero EV Means Safe”

One persistent misconception is that a near-zero expected value implies low risk. This interpretation is incorrect. Expected value measures average outcome, not exposure to extreme paths.

In a Martingale system, progression mechanics amplify variance. Small deviations early in a sequence can lead to large state changes later. When combined with finite resources, this amplification creates significant tail risk regardless of expectation.

The belief that near-zero expectation implies safety arises because expectation is mistaken for stability. In reality, stability is governed by variance and boundary conditions, not by average outcomes. This misunderstanding is widespread because expected value is often presented without context. In isolation, it appears reassuring. Within a progression model, it is not.

Relationship Between Expected Value and Risk of Ruin

Expected value and risk of ruin describe different aspects of the same system. Expected value characterizes long-run averages. Risk of ruin describes the probability that a finite system reaches an absorbing boundary.

In a Martingale system with a finite bankroll, negative expected value combined with exponential progression leads to a non-zero probability of absorption. Expected value does not prevent this outcome. It does not delay it. It does not mitigate it.

This relationship is formalized in the discussion of risk of ruin, which explains how finite boundaries dominate long-run expectation. Expected value operates in theory. Absorbing boundaries operate in practice. For a full structural explanation, see the constraint page on Risk of Ruin in Martingale Systems.

Expected Value Under Infinite Versus Finite Horizons

Expected value is defined asymptotically. It assumes an infinite number of trials. Under this assumption, averages converge and expectation becomes observable.

Real systems do not operate under infinite horizons. They terminate. They encounter limits. They stop long before asymptotic behavior emerges. This difference is not incidental. It is fundamental.

In a finite system, expected value remains mathematically valid but practically unrealized. The system ends before convergence. Outcomes are dominated by variance and boundary effects rather than averages. This distinction explains why expected value cannot be used as a practical descriptor of finite Martingale behavior. The theory assumes conditions that finite systems cannot satisfy.

What the Martingale Calculator Shows About Expected Value

The Martingale Calculator does not compute expected value directly. Its purpose is not to display expectation as a metric. Instead, it illustrates how expectation interacts with variance and finite constraints.

The simulation output shows distributional behavior. It reveals how often boundaries are reached and how progression depth evolves under stated assumptions. Expected value is implicit in the model, not displayed as a target.

This distinction is intentional. Displaying expected value without context would invite misinterpretation. The calculator is designed to remain descriptive, not evaluative.

To understand why the calculator is framed this way, see Martingale Systems as Mathematical Models.

Why Expected Value Must Be Read as a Constraint, Not a Goal

Expected value functions as a boundary on interpretation. It tells us what a model averages to under idealized repetition. It does not define objectives and it does not suggest targets.

Treating expected value as something to be pursued leads to misuse. It shifts attention away from variance, termination, and finite limits. In Martingale systems, these factors dominate behavior.

Within this project, expected value is treated as a constraint. It limits what can be inferred. It prevents certain conclusions from being drawn. It does not justify action or configuration. This hierarchy is deliberate. Expected value constrains interpretation. It does not direct it.

Summary

-

Expected value is a mathematical average defined over repeated trials.

-

It does not describe individual outcomes or short sequences.

-

It does not remove variance or tail risk.

-

It does not override finite bankroll constraints.

-

In Martingale systems, expected value must be read as a structural property, not as a goal.

This page constrains how all expected-value-related outputs on this site must be interpreted.